Issuing an invoice correctly in the buying and selling of used cars is not just a legal obligation: it is a guarantee of professionalism, transparency and tax security. If you are a dealer or a professional in the sector, this step-by-step guide will help you understand what type of invoice you should issue in each case, how to calculate VAT according to the applicable scheme (REBU or standard), what information it must contain and what mistakes you should avoid.

Who must issue an invoice in the buying and selling of used vehicles?

Professional dealers vs sales between private individuals

Only professional sellers (self-employed traders or companies dedicated to buying and selling) are required to issue an invoice. In sales between private individuals, no invoice is issued, but rather a private sale and purchase contract, and neither VAT nor REBU applies. For dealers, issuing an invoice is mandatory in all transactions.

Tax obligations of a buy-and-sell business

As a professional in the sector, you are required to:

Issue an invoice for every sale

Number and retain the invoices issued

Record transactions in the accounting books

Declare output VAT or the REBU margin in forms 303 and 390

Is it mandatory to issue an invoice if I sell to a private individual?

Yes. Even if the buyer is a private customer, the regulations require the professional seller to issue an invoice that correctly reflects the type of transaction and the tax scheme applied.

Types of invoicing according to the type of transaction

Sale with VAT (Standard scheme)

This scheme applies when the dealer acquires the vehicle from a company or another professional with the right to deduct VAT. In this case, VAT is calculated on the total sale price and itemised on the invoice. It is common in fleet, leasing or renting transactions.

Sale under REBU (Special Scheme for Used Goods)

REBU applies when the vehicle is acquired from a private individual or another professional who does not deduct VAT. In this case:

VAT is calculated on the margin (sale price - purchase price + associated non-deductible expenses)

It is not itemised on the invoice

Deduction of input VAT is not allowed

This scheme is the most common for dealers buying used cars from private individuals.

Intra-EU sale or import

If the car is bought in another EU country:

If the supplier is a company with an intra-EU VAT number, the reverse charge mechanism can be applied (no VAT on the invoice, but self-assessment on form 303)

If the supplier is a private individual, REBU can be applied

It is essential to declare the transaction correctly on form 349 and keep the transport documentation and taxes paid.

Special cases

Internal use or demonstrator vehicles: may generate VAT adjustments due to self-supply

Financed vehicles: the invoice shows the total price; financing is a separate contract

Renting or leasing with an option to buy: require specific tax treatment; they are not direct sales

How to make out an invoice correctly (step by step)

Mandatory details on every invoice

Full name or company name of the buyer and the seller

Tax ID/VAT number and registered address of both parties

Date of issue

Invoice number (sequential, with no gaps)

Detailed description of the vehicle (make, model, registration plate, chassis number, mileage, year of registration)

Net price, VAT (if applicable) or REBU margin

Payment method

Reference to the tax scheme (REBU, standard, exempt)

Invoice with VAT (Standard scheme)

It must show the taxable base and the VAT rate (normally 21%)

State "Transaction subject to and not exempt from VAT"

The buyer can deduct the VAT if they are a company or professional

Invoice with REBU

VAT is not itemised

The following wording must be included:

"Special scheme for used goods. VAT included in the price. Not deductible."

The margin must be calculated internally in order to declare it correctly

Record book

You must keep:

Invoice issued ledger

Purchase ledger (if VAT applies)

REBU transactions ledger, if you use this scheme, including:

Purchase price

Sale price

Gross margin

VAT calculated on the margin (for declaration only, not on the invoice)

Practical invoicing examples

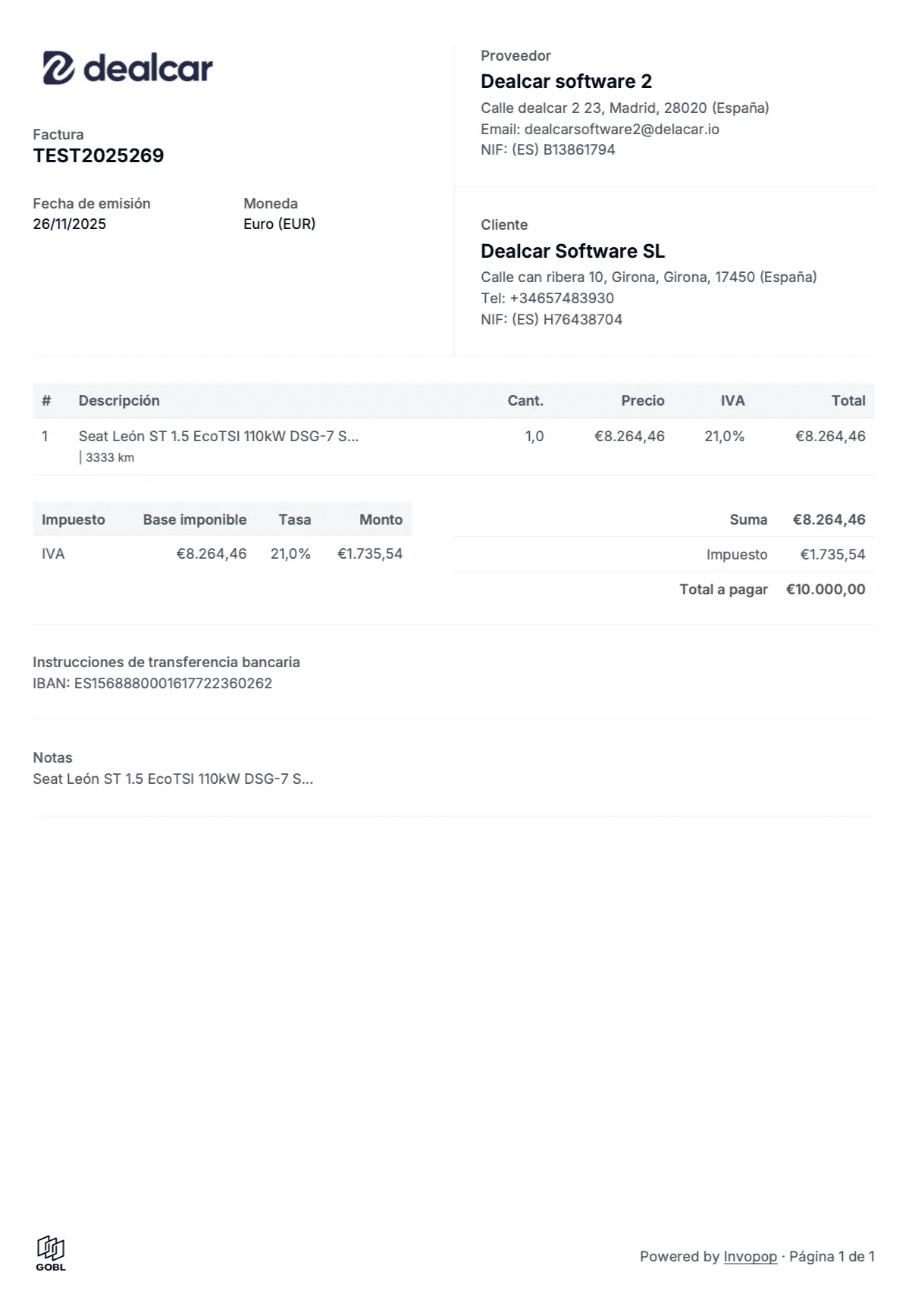

Invoice with VAT (sale to a company)

Invoice:

Base price: €10,000

VAT (21%): €2,100

Total invoice: €12,100

The buyer can deduct that VAT if they are a company.

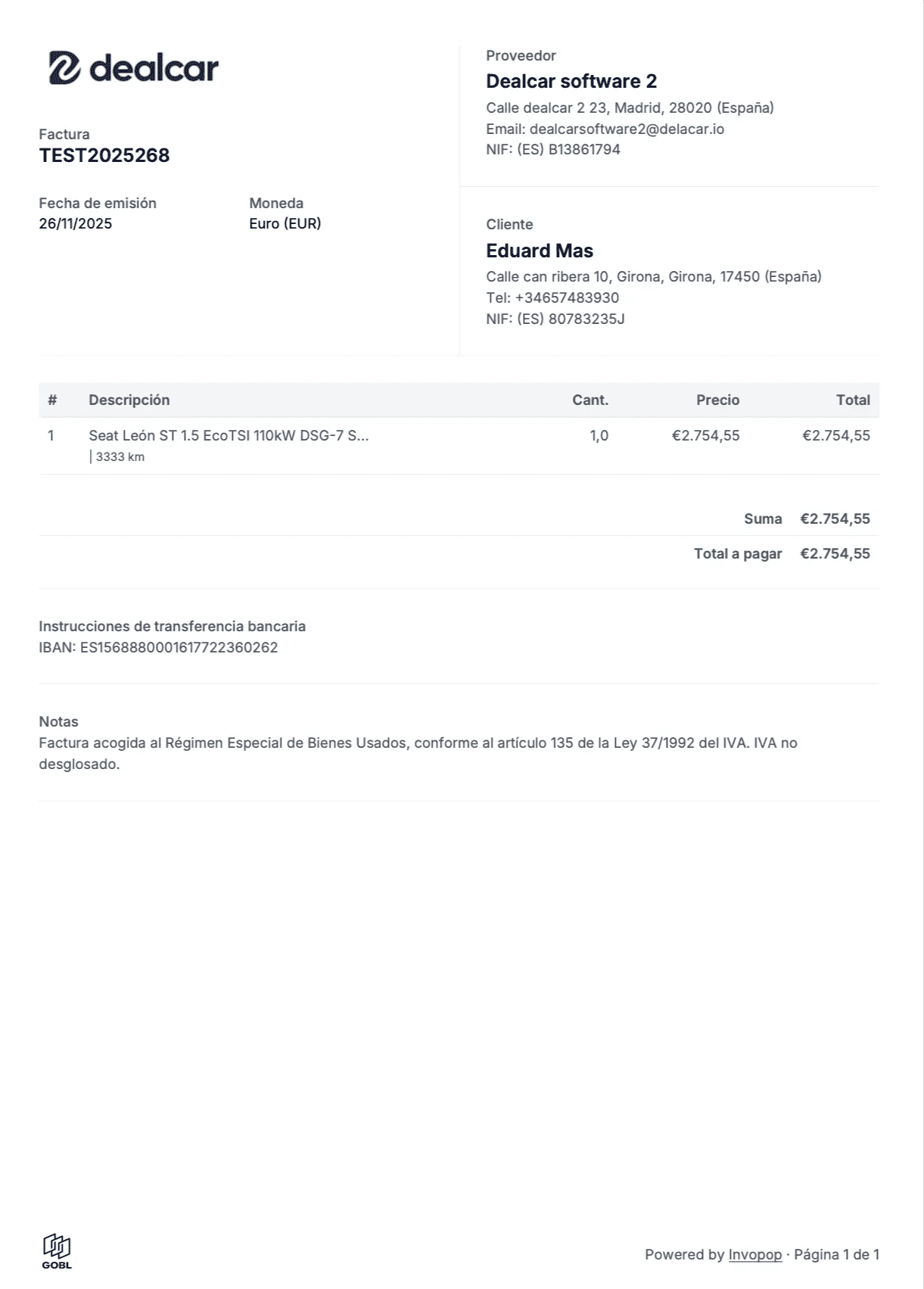

Invoice with REBU (sale to a private individual)

Invoice:

Sale price: €10,000 (VAT included on the margin)

Wording: "REBU. VAT included. Not deductible."

No VAT breakdown appears

Invoice for an imported car (intra-EU transaction)

If you apply REBU: the same as a purchase from a private individual

If you apply VAT: you must self-assess on form 303 and declare on form 349

Discover our complete REBU guide for more details.

Common mistakes when issuing invoices in buy-and-sell businesses

Confusing the tax scheme

Applying VAT when REBU should apply (and vice versa)

Using REBU for purchases with the right to deduct

Omitting mandatory details

Incomplete customer or vehicle details

Not stating the tax scheme

Incorrect invoice numbering

Declaring VAT incorrectly

Under REBU: VAT is calculated only on the margin

Declaring the total as the taxable base can cause errors and penalties

Using the same invoice for several transactions

Each vehicle must have its own invoice, with a unique identifier. Avoid grouped invoices.

Tips for dealers: professionalise your invoicing

Use tailored templates

Having specific templates for REBU and VAT avoids confusion and conveys professionalism. Dealcar offers ready-to-use templates.

Automate the process

If you have volume, consider using management or invoicing software that allows you to:

Generate automatic invoices

Keep a record of purchases and sales

Export data for filing tax returns

Consult your tax adviser

The combination of the standard scheme, REBU and intra-EU transactions requires professional attention to avoid mistakes and tax authority penalties.

Learn more about REBU

Do you have questions about how this special scheme works? Check out our complete REBU guide for dealers.

Conclusion

Issuing an invoice properly is not just about complying with the tax authorities, but also about demonstrating professionalism and protecting your business against possible claims. If you apply REBU correctly, declare your income clearly and use validated templates, you will be one step ahead of the competition.

At Dealcar we help you simplify your dealership's day-to-day management with tools, templates and up-to-date content for professionals like you. Check out our invoicing templates and take your business's tax control to the next level!

Issuing an invoice correctly in the buying and selling of used cars is not just a legal obligation: it is a guarantee of professionalism, transparency and tax security. If you are a dealer or a professional in the sector, this step-by-step guide will help you understand what type of invoice you should issue in each case, how to calculate VAT according to the applicable scheme (REBU or standard), what information it must contain and what mistakes you should avoid.

Who must issue an invoice in the buying and selling of used vehicles?

Professional dealers vs sales between private individuals

Only professional sellers (self-employed traders or companies dedicated to buying and selling) are required to issue an invoice. In sales between private individuals, no invoice is issued, but rather a private sale and purchase contract, and neither VAT nor REBU applies. For dealers, issuing an invoice is mandatory in all transactions.

Tax obligations of a buy-and-sell business

As a professional in the sector, you are required to:

Issue an invoice for every sale

Number and retain the invoices issued

Record transactions in the accounting books

Declare output VAT or the REBU margin in forms 303 and 390

Is it mandatory to issue an invoice if I sell to a private individual?

Yes. Even if the buyer is a private customer, the regulations require the professional seller to issue an invoice that correctly reflects the type of transaction and the tax scheme applied.

Types of invoicing according to the type of transaction

Sale with VAT (Standard scheme)

This scheme applies when the dealer acquires the vehicle from a company or another professional with the right to deduct VAT. In this case, VAT is calculated on the total sale price and itemised on the invoice. It is common in fleet, leasing or renting transactions.

Sale under REBU (Special Scheme for Used Goods)

REBU applies when the vehicle is acquired from a private individual or another professional who does not deduct VAT. In this case:

VAT is calculated on the margin (sale price - purchase price + associated non-deductible expenses)

It is not itemised on the invoice

Deduction of input VAT is not allowed

This scheme is the most common for dealers buying used cars from private individuals.

Intra-EU sale or import

If the car is bought in another EU country:

If the supplier is a company with an intra-EU VAT number, the reverse charge mechanism can be applied (no VAT on the invoice, but self-assessment on form 303)

If the supplier is a private individual, REBU can be applied

It is essential to declare the transaction correctly on form 349 and keep the transport documentation and taxes paid.

Special cases

Internal use or demonstrator vehicles: may generate VAT adjustments due to self-supply

Financed vehicles: the invoice shows the total price; financing is a separate contract

Renting or leasing with an option to buy: require specific tax treatment; they are not direct sales

How to make out an invoice correctly (step by step)

Mandatory details on every invoice

Full name or company name of the buyer and the seller

Tax ID/VAT number and registered address of both parties

Date of issue

Invoice number (sequential, with no gaps)

Detailed description of the vehicle (make, model, registration plate, chassis number, mileage, year of registration)

Net price, VAT (if applicable) or REBU margin

Payment method

Reference to the tax scheme (REBU, standard, exempt)

Invoice with VAT (Standard scheme)

It must show the taxable base and the VAT rate (normally 21%)

State "Transaction subject to and not exempt from VAT"

The buyer can deduct the VAT if they are a company or professional

Invoice with REBU

VAT is not itemised

The following wording must be included:

"Special scheme for used goods. VAT included in the price. Not deductible."

The margin must be calculated internally in order to declare it correctly

Record book

You must keep:

Invoice issued ledger

Purchase ledger (if VAT applies)

REBU transactions ledger, if you use this scheme, including:

Purchase price

Sale price

Gross margin

VAT calculated on the margin (for declaration only, not on the invoice)

Practical invoicing examples

Invoice with VAT (sale to a company)

Invoice:

Base price: €10,000

VAT (21%): €2,100

Total invoice: €12,100

The buyer can deduct that VAT if they are a company.

Invoice with REBU (sale to a private individual)

Invoice:

Sale price: €10,000 (VAT included on the margin)

Wording: "REBU. VAT included. Not deductible."

No VAT breakdown appears

Invoice for an imported car (intra-EU transaction)

If you apply REBU: the same as a purchase from a private individual

If you apply VAT: you must self-assess on form 303 and declare on form 349

Discover our complete REBU guide for more details.

Common mistakes when issuing invoices in buy-and-sell businesses

Confusing the tax scheme

Applying VAT when REBU should apply (and vice versa)

Using REBU for purchases with the right to deduct

Omitting mandatory details

Incomplete customer or vehicle details

Not stating the tax scheme

Incorrect invoice numbering

Declaring VAT incorrectly

Under REBU: VAT is calculated only on the margin

Declaring the total as the taxable base can cause errors and penalties

Using the same invoice for several transactions

Each vehicle must have its own invoice, with a unique identifier. Avoid grouped invoices.

Tips for dealers: professionalise your invoicing

Use tailored templates

Having specific templates for REBU and VAT avoids confusion and conveys professionalism. Dealcar offers ready-to-use templates.

Automate the process

If you have volume, consider using management or invoicing software that allows you to:

Generate automatic invoices

Keep a record of purchases and sales

Export data for filing tax returns

Consult your tax adviser

The combination of the standard scheme, REBU and intra-EU transactions requires professional attention to avoid mistakes and tax authority penalties.

Learn more about REBU

Do you have questions about how this special scheme works? Check out our complete REBU guide for dealers.

Conclusion

Issuing an invoice properly is not just about complying with the tax authorities, but also about demonstrating professionalism and protecting your business against possible claims. If you apply REBU correctly, declare your income clearly and use validated templates, you will be one step ahead of the competition.

At Dealcar we help you simplify your dealership's day-to-day management with tools, templates and up-to-date content for professionals like you. Check out our invoicing templates and take your business's tax control to the next level!